Thursday, May 28, 2015

Saturday, May 23, 2015

Wednesday, May 20, 2015

Sunday, May 17, 2015

Thursday, May 14, 2015

Home Prices: "RED ALERT 2" MUST READ. Worse than 2008?

"...Real Estate is a highly “illiquid” asset class ‘most of the time’. It always has been and always will be. However, some times, such as now — and from 2003 to 2007 as a prime example — when liquidity is flowing like water, Real Estate’s illiquidity is masked. Speculators can do no wrong. Simply having access to short-term or mortgage capital to purchase Real Estate guaranties a double-digit return.

This continues until one day, suddenly, it doesn’t. When capital markets tighten up a bit, or a lot, due to one reason, another, or another, the snap-back to the true, historical illiquid nature of the Real Estate sector happens suddenly and is amplified at first. This creates a snowball effect from which both house supply and illiquidity surge at the same time.

This continues until one day, suddenly, it doesn’t. When capital markets tighten up a bit, or a lot, due to one reason, another, or another, the snap-back to the true, historical illiquid nature of the Real Estate sector happens suddenly and is amplified at first. This creates a snowball effect from which both house supply and illiquidity surge at the same time.

Price then becomes the liquidity fulcrum and will drop, relentlessly ripping speculators faces off, until capital begins to view the asset class as a relative value once again.

In periods of mania, most don’t recognize when Real Estate has once again lost its levitation juice and keep buying even as liquidity conditions turn downright bearish. Some buy all the way down comparing the lower prices with peak, liquidity bubble prices a couple of quarters back thinking they are getting a “great deal”. Quickly, they are underwater, or sinking rehab capital into a depreciating asset.

Then, what seems like “all of a sudden”, a wave of fear engulfs the sector. Supply ratchets higher, as pricing power continues to weaken. Before most realize what’s happening, “month’s supply” of houses is ‘through the roof’, Realtors are telling sellers that their ‘expectations are a bit high’, and Real Estate’s true color — illiquidity — has taken control of the entire sector stranding owners and speculators from their invested capital. This is event horizon.

These “correction” cycles can be tame, moderate, or extreme like from 2003 to 2007. In my opinion the severity of the correction is directly related to the amount energy that preceded it, meaning given the “all-in” global Central Bank monetary and Gov’t debt policies of the past 6-years, the next “correction” has the potential to make 2007 to 2010 look moderate..."

SACRIFICE! Read this: http://mhanson.com/archives/1788

“Beware of security as a goal. It may often look like life’s best prize. Usually it is not.” — RIP William Zinsser.

“Ultimately, the product any writer has to sell is not the subject being written about, but who he or she is,” Mr. Zinsser wrote in “On Writing Well.” He added: “I often find myself reading with interest about a topic I never thought would interest me — some scientific quest, perhaps. What holds me is the enthusiasm of the writer for his field.”

...“Abraham Lincoln and Winston Churchill rode to glory on the back of the strong declarative sentence,” he wrote in “Writing to Learn: How to Write — and Think — Clearly About Any Subject at All” (1988)..."

READ THE WHOLE THING!

http://www.nytimes.com/2015/05/13/arts/william-zinsser-author-of-on-writing-well-dies-at-92.html?ref=obituaries&_r=0

...“Abraham Lincoln and Winston Churchill rode to glory on the back of the strong declarative sentence,” he wrote in “Writing to Learn: How to Write — and Think — Clearly About Any Subject at All” (1988)..."

READ THE WHOLE THING!

http://www.nytimes.com/2015/05/13/arts/william-zinsser-author-of-on-writing-well-dies-at-92.html?ref=obituaries&_r=0

Tuesday, May 12, 2015

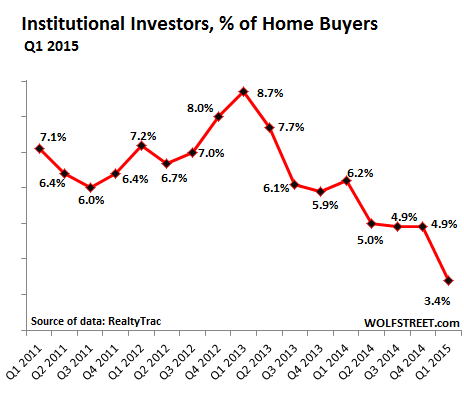

Rental Armageddon Continues...

"...smaller investors…purchasing <10 properties/yr are getting INTO the game while the bigger players back OUT. The television ads and radio shows are now screaming (for a few years now) how awesome it is to get into the flip/sell/buy real estate game..." (See link, below graphs.)

http://www.doctorhousingbubble.com/rental-armageddon-continues-net-worth-up-at-higher-end-driven-by-housing-hot-money/

http://www.doctorhousingbubble.com/rental-armageddon-continues-net-worth-up-at-higher-end-driven-by-housing-hot-money/

Monday, May 11, 2015

"...commodity rally...too far/too fast...steep dnwd…warning...investors across all asset[s] monitor closely."

"...The first half of Q2 has seen a strong rally develop in commodities prices. Brent crude oil is up 24% (after performing flat in Q1), copper 12% and even gold has risen a little. Despite the fact that agricultural commodities and livestock prices have continued to be weak, the S&PGSCI spot price index has made its best start to a year since 2011, up 8% in the year-to-date.

Although the price rebound is directly benefitting commodity index investors much less then the spot price gains might suggest (because the high cost of carry has reduced total returns), the strength of the commodity recovery is greatly influencing global growth expectations and movements in other asset classes.

- Just as the steep decline in oil prices in late 2014 kicked-off concerns about the health of the global economy, the recovery is being viewed by some market observers as a strong indicator that growth prospects may be improving faster than markets had expected, especially as it is heavily focused on energy and industrial metals.

- The recovery in oil prices, in particular, is helping to allay concerns that important parts of the global economy might slip into a deflationary spiral. As investors have become more confident about the future (or at least less pessimistic), many of the deflation-axed positions built up earlier this year, especially in fixed income markets, are being unwound.

Consequently, the commodity price rally has been an important influence on the recent pickup in global bond yields.Although these remain low versus historical levels some of the recent action has been eye-catching (US 10y treasury yields and the 10y BUND are both up about 45bp since mid-April, to reach year-to-date highs) and it is hard to imagine that the moves would have been quite as aggressive without the big move up in commodities, particularly oil.

So for many reasons the answer to the question: “will the commodity price rally continue?” is particularly important at this juncture. Our view is that it will prove very tough to make further significant gains in commodity prices from here unless supply/demand conditions improve very fast indeed. In our view, prices for key commodities like oil, copper and gold, have already hit levels that would not be justified until later in H2, ie, following a longer sustained period of improving fundamentals than we have seen in H1 to date.

Indeed the risks are growing that the commodity price rally has moved too far ahead, too fast and that a steep downward adjustment could be just around the corner. In our view, there are several warning signs in commodities markets that we would advise investors across all asset classes to monitor closely.

http://www.zerohedge.com/news/2015-05-11/huge-disconnect-between-physical-futures-suggests-commodity-rally-wont-last-barclaysChina looks fragile. China’s commodity demand has had a reasonably strong start to the year with oil demand up 7.2% and copper up 4% in Q1. However, these figures are at odds with downbeat IP data (Figure 3) and imports have probably been boosted by stockpiling, especially for strategic commodities like oil and copper. April data released on Friday showed reasonably healthy import levels for these two commodities, but iron ore and soybeans were weak. The risk is that domestic demand and commodity imports could fall back as Q2 progresses.Supply is still exceeding consumption. In particular, it still does not appear that the supply cuts necessary to balance the oil market are being made fast enough. Although there has been some slowing in the rate of US supply growth and a rapid decline in the rig count, offsetting that is the fact OPEC production has risen by 500kb/d since the start of the year to 31m b/d. If OPEC maintains that output level through Q2, then even with a further slowing in US oil production, the oil balances of the major forecasting agencies (and our own) indicate that global oil stocks will rise more quickly in Q2 than in Q1 (Figure 4) and to continue climbing through to year-end at least.The oil price recovery may encourage some US producers to restart. EOG, often viewed as one of the best positioned independent US shale oil companies, said this week that if oil prices “stabilise at the $65 level” (less than 10% above current levels) it is prepared for “strong double digit” output growth in 2016. Moreover, the flattening of the WTI futures curve will add to the incentive for producers to gradually bring on drilled, but uncompleted wells. Neither the current trajectory of oil prices nor production looks sustainable to us in such a scenario. Something will have to give.Finally there is a huge disconnect between price action in physical markets where differentials are signalling oversupply and futures markets where all looks rosy. Financial drivers have been key in this commodity rally, with short-covering driving part of it, but fresh longs being drawn in. Net speculative length in Brent crude has doubled since the start of the year to its highest level since data collection began in 2011. In copper the LME net long position has grown by 60% since the start of the year and on COMEX copper, speculators have swung rapidly from short to long… ."

Sunday, May 10, 2015

Fundamentals?? "We currently have over 93 Million able-bodied people without jobs – and growing..."

Goldilocks Unemployment: A Disgusting Bowl Of Porridge

by Mark St.Cyr • May 10, 2015"It’s no wonder we find ourselves in this collective business environment of malaise and atrophy when people who are supposed to be informed, or anything else relating to business, use terms to describe the most recent jobs report as a “Goldilocks” print: i.e., “Not too bad – Not too good.”

This term was the moniker de jure of Friday’s cadre of financial media economists, analysts, and next in rotation fund manager. Nothing more than cheerleaders to stagflation is what they’ve all proven themselves to be in my opinion than anything else.

The actual print was that the economy created 223K new jobs vs expectations of 228K. Where the overall jobless rate now stands at 5.4 vs 5.5. The kicker? Not in the labor force: 93,194,000 up from 93,175,000. Let that last number sink in a moment.

We currently have over 93 Million able-bodied people without jobs – and growing. This is why it’s near incomprehensible, as well as outright disgusting to me that such a dismal showing in both the headline number as well as the onerous implications of such a downward revision to the month prior, coupled with the outright fallacy of suggesting the rate of unemployment has moved closer still to statistical “full employment” came with near giddiness and if not outright back slapping. i.e., “This is a Goldilocks print. Not too hot – not too cold. With a report like this – The Federal Reserve won’t dare raise rates and might actually have to contemplate instituting another round of QE if not outright QE4ever!” And yes; that was the reaction paraphrased across the financial media outlets. Again, personally – I found it all repulsive.

We now have the lowest participation rate since 1977 when Jimmy Carter was president. Although I was young during that period, I was around and working. (and when I wasn’t working, I was out looking daily) I will tell you this: one of the words never bandied about during that period when it came to describe any jobs or employment report was “Goldilocks.”... ."

http://markstcyr.com/2015/05/10/goldilocks-unemployment-a-disgusting-bowl-of-porridge/

Friday, May 8, 2015

Tuesday, May 5, 2015

Economic Perspective...for the Thoughful. REAL data.

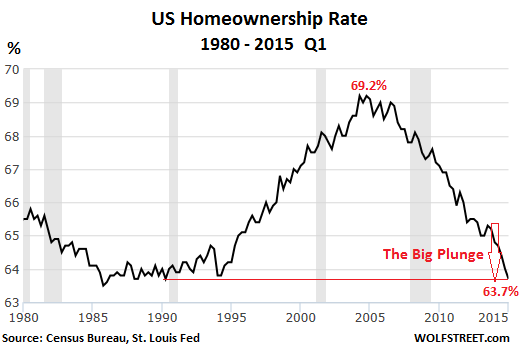

We have the employment to population ratio at 35 year lows. We have had stagnant real wage growth since 2008 as low paying service Obama jobs have replaced higher paying production jobs. We have real median household income at 1989 levels and still 9% below the 2008 peak. We have mortgage applications 56% below the 2005 peak and hovering at 1996 levels. We still have 4 million homeowners underwater in their mortgages. We have housing starts languishing 40% below the long-term average. We have the home ownership rate of 63.8% at quarter of a century lows. We have mortgage rates at all-time lows. And we have home prices soaring far above the inflation rate and wages because the Federal Reserve, in collaboration with the Federal government decided to create another housing bubble (along with stock and bond bubbles) to rectify the disastrous consequences of their last housing bubble.

Monday, May 4, 2015

.jpg)

Friday, May 1, 2015

Fed "Bound And Determined" To Engineer "Full-Fledged Bubble"

Jeremy Grantham: "I still believe that before this cycle ends, the quantity of U.S. deals, including co- investments, should rise to a record given the unprecedented low rates and the current extreme reluctance to make new investments in plant and equipment (how old-fashioned that sounds these days) rather than into stock buybacks, which may be good for corporate officers and stockholders, but bad for GDP growth and employment and, hence, wages."

http://www.zerohedge.com/news/2015-05-01/grantham-says-fed-bound-and-determined-engineer-full-fledged-bubble

Subscribe to:

Posts (Atom)